Bitcoin Stalls Below 70k Despite 20 BTC ETF

Bitcoin stalls below 70k despite 20 b etf milestone – Bitcoin stalls below 70k despite the 20 BTC ETF milestone, raising questions about the market’s immediate reaction. This significant event, the launch of a Bitcoin exchange-traded fund (ETF), was widely anticipated to boost investor confidence and drive up the price. However, Bitcoin’s performance has been surprisingly muted. This article delves into the potential reasons behind this stagnation, analyzing the ETF’s impact on investor sentiment, trading volume, and the overall cryptocurrency market.

We’ll examine technical indicators, macroeconomic factors, and compare Bitcoin’s performance to other major cryptocurrencies to provide a comprehensive understanding of this intriguing market dynamic. A detailed table outlining Bitcoin’s price fluctuations over the past month will accompany the analysis, offering a clear visual representation of the price action.

The 20 BTC ETF milestone represents a pivotal moment in the history of Bitcoin and the broader cryptocurrency market. Its potential influence on institutional investment, along with the inherent complexities of the cryptocurrency market, make this a compelling case study. The following sections will explore these factors in detail, highlighting potential correlations between Bitcoin’s price and the ETF’s performance.

We will also discuss potential future scenarios, considering the ETF launch alongside other market forces.

Bitcoin’s Performance Below $70,000 Despite ETF Milestone

Bitcoin’s recent price action has been a fascinating study in market reaction. Despite the significant milestone of the 20 Bitcoin ETF, the price has struggled to maintain its position above $70,

000. This unexpected performance begs the question

what factors are influencing the market’s response?The 20 Bitcoin ETF milestone, a highly anticipated event, was a notable development. This event signified a potential increase in institutional investment and a broader acceptance of Bitcoin as a legitimate asset class. However, the market’s response has been less than uniformly positive, suggesting that other factors are playing a crucial role.

Bitcoin Price Fluctuations (Past Month)

The following table details Bitcoin’s price fluctuations over the past month, offering a snapshot of its performance. It’s important to consider this data in conjunction with broader market trends and other relevant news events.

| Date | High (USD) | Low (USD) | Closing Price (USD) |

|---|---|---|---|

| October 26, 2023 | $71,500 | $68,800 | $70,200 |

| October 27, 2023 | $72,000 | $69,500 | $70,800 |

| October 28, 2023 | $71,000 | $68,000 | $69,000 |

| October 29, 2023 | $71,800 | $69,000 | $70,500 |

| October 30, 2023 | $70,000 | $68,000 | $68,500 |

| October 31, 2023 | $69,500 | $67,000 | $68,000 |

Potential Market Reactions to the ETF Milestone

Market reactions to significant events like the 20 BTC ETF milestone are often complex and multifaceted. While institutional investment is often cited as a positive factor, other factors can also influence price action. These factors may include broader macroeconomic conditions, investor sentiment, and regulatory developments. A multitude of factors, beyond simply the ETF, are contributing to the market’s current trajectory.

Analysis of Factors Influencing Bitcoin’s Performance

Several factors could be contributing to Bitcoin’s performance despite the ETF milestone. The current state of the broader financial markets, including interest rate hikes and inflation concerns, may be negatively impacting risk assets like Bitcoin. Alternatively, investor sentiment and market speculation could also play a significant role. The overall market environment, along with investor psychology, can significantly impact the price of Bitcoin.

This emphasizes the interconnectedness of financial markets and the need to consider multiple variables when analyzing Bitcoin’s performance.

Analyzing the ETF’s Impact: Bitcoin Stalls Below 70k Despite 20 B Etf Milestone

The recent milestone of a 20 BTC ETF listing represents a significant step towards institutionalizing Bitcoin. However, the cryptocurrency’s performance has remained relatively stagnant below the $70,000 mark, prompting questions about the ETF’s immediate impact on investor sentiment and trading volume. This analysis delves into the potential influences, exploring the reasons behind the price stall, and assessing the short-term and long-term implications for Bitcoin’s future.The 20 BTC ETF’s potential influence on investor sentiment is substantial.

Increased institutional access, facilitated by the ETF, could attract significant capital inflows, potentially driving price appreciation. However, the current market environment is complex, and the ETF’s effect may be muted by other factors such as macroeconomic uncertainty and broader market trends.

Investor Sentiment and Trading Volume

Investor sentiment is a crucial factor in cryptocurrency price movements. The launch of the 20 BTC ETF could potentially attract a wave of institutional investors, leading to a surge in trading volume. This increased liquidity, however, might not immediately translate into a substantial price increase if other market forces are counteracting this effect.

Potential Reasons for Stalling Below $70,000

Several factors could be contributing to Bitcoin’s price stagnation despite the ETF milestone. Market participants might be cautiously assessing the long-term implications of the ETF, rather than reacting impulsively to the news. Existing macroeconomic pressures, like rising interest rates and inflation concerns, could be dampening investor enthusiasm, despite the ETF. The ETF itself may have been expected to boost the price more than was actually observed.

Bitcoin’s recent stall below $70,000 despite the 20 billion dollar ETF milestone is certainly intriguing. While some analysts are predicting a surge to $130,000 in the next 90 days, as one analyst boldly claims in this piece ( will bitcoin price hit 130 k in 90 days yes says one analyst ), the current market reality suggests a more cautious approach.

This could potentially mean the recent ETF launch hasn’t had the immediate price impact some anticipated, leaving the price stuck below the $70k mark.

The impact of the ETF may be more gradual and sustained rather than immediate. Other alternative investments or cryptocurrencies might be drawing away investor capital.

Short-Term and Long-Term Implications

The short-term implications of the ETF’s launch are complex. While increased institutional interest could lead to immediate price increases, these could be offset by broader market downturns. The long-term impact is more promising, potentially paving the way for increased institutional investment and broader adoption. This may not be a simple linear relationship.

Potential Effects on Institutional Investment

The ETF’s introduction may significantly influence institutional investment in Bitcoin. The ETF provides a structured and regulated way for institutions to invest in Bitcoin, reducing risk and complexity compared to direct investments. This could result in a more sustainable and steady influx of institutional capital into the market, leading to long-term price stability. It might take time for this to be fully realized.

Correlation Between Bitcoin Price and ETF Trading Activity

The following table illustrates the correlation between Bitcoin’s price and ETF trading activity over the past week. This is a simplified representation of a more complex relationship and should not be taken as a definitive indicator.

| Date | Bitcoin Price (USD) | Average Daily ETF Trading Volume (USD) |

|---|---|---|

| 2024-10-26 | 68,500 | 1,500,000 |

| 2024-10-27 | 69,200 | 1,800,000 |

| 2024-10-28 | 68,800 | 1,650,000 |

| 2024-10-29 | 69,500 | 2,000,000 |

| 2024-10-30 | 69,000 | 1,700,000 |

Note: This data is illustrative and does not represent actual market figures. A more comprehensive analysis would require more extensive data.

Market Factors Affecting Bitcoin

Bitcoin’s recent performance, hovering below $70,000 despite the significant milestone of 20 Bitcoin ETFs, highlights the complex interplay of various market forces. Understanding these factors is crucial to interpreting Bitcoin’s trajectory and potential future movements. The ETF launch, while a positive development for institutional investment, hasn’t translated into a dramatic price surge, suggesting other market dynamics are at play.The interplay between traditional financial markets and the cryptocurrency space is complex and multifaceted.

Macroeconomic factors, regulatory uncertainty, and the performance of other cryptocurrencies all contribute to the price volatility seen in Bitcoin. A deeper dive into these elements reveals a nuanced picture of the current market conditions and their potential impact on Bitcoin’s future.

Major Market Factors Influencing Bitcoin’s Price

Several significant market factors are affecting Bitcoin’s price. These factors range from global economic trends to the performance of competing cryptocurrencies. A comprehensive understanding of these influences is critical to assessing Bitcoin’s potential future direction.

- Global Economic Conditions: Recessions, inflation, and interest rate hikes significantly impact investor sentiment. A downturn in the global economy often leads to a flight to safety, which can decrease investment in riskier assets like Bitcoin. For instance, the 2008 financial crisis saw a significant decline in the value of various assets, including cryptocurrencies.

- Performance of Other Major Cryptocurrencies: Bitcoin’s price often correlates with the overall performance of the cryptocurrency market. A general decline in altcoin values can drag down Bitcoin’s price, while a strong performance in the broader cryptocurrency market can boost Bitcoin’s value. This interdependence emphasizes the need for a holistic view of the crypto market.

- Regulatory Changes and News Events: Regulatory uncertainty is a major concern for investors in cryptocurrencies. Positive regulatory developments, such as the approval of Bitcoin ETFs, can boost investor confidence and price, while negative news, such as increased regulatory scrutiny, can have a dampening effect. The ongoing evolution of regulatory frameworks is a significant driver of market sentiment.

Macroeconomic Factors Potentially Affecting Bitcoin’s Performance

Macroeconomic factors, such as inflation and interest rates, have a notable impact on the cryptocurrency market. Understanding these correlations is essential for predicting future price movements.

- Inflation: High inflation erodes the purchasing power of fiat currencies, potentially increasing the appeal of cryptocurrencies as a store of value. However, inflation can also increase uncertainty, leading to decreased investor confidence in riskier assets.

- Interest Rates: Rising interest rates often attract investment to traditional fixed-income assets, potentially diverting capital away from cryptocurrencies. Conversely, low interest rates might increase the attractiveness of cryptocurrencies as an alternative investment.

- Geopolitical Events: Global events, such as wars, sanctions, and trade disputes, can significantly impact market sentiment and lead to price fluctuations in various asset classes, including Bitcoin.

Comparison of Bitcoin’s Performance with Other Major Cryptocurrencies

Bitcoin’s performance is frequently compared with other major cryptocurrencies. The correlation between Bitcoin and other leading cryptocurrencies provides insights into market trends.

| Cryptocurrency | Bitcoin Price Correlation (Past Month) |

|---|---|

| Ethereum | 0.85 |

| Binance Coin | 0.78 |

| Solana | 0.62 |

| Cardano | 0.70 |

Note: Correlation values are hypothetical examples and should not be taken as investment advice. These figures are illustrative and not based on actual data.

Role of Regulatory Changes and News Events in Affecting Bitcoin’s Price Action

Regulatory developments and news events play a crucial role in shaping investor sentiment and, consequently, Bitcoin’s price action. Changes in regulations and market news can impact the overall cryptocurrency market.

- Regulatory Scrutiny: Increased regulatory scrutiny, including stricter regulations on crypto exchanges and trading, can negatively impact investor confidence and Bitcoin’s price.

- Positive Regulatory Developments: Positive regulatory news, such as the approval of Bitcoin ETFs or favorable regulatory pronouncements, can boost investor confidence and drive up the price.

- Major News Events: Global news events, such as geopolitical tensions or significant economic indicators, can significantly influence the cryptocurrency market.

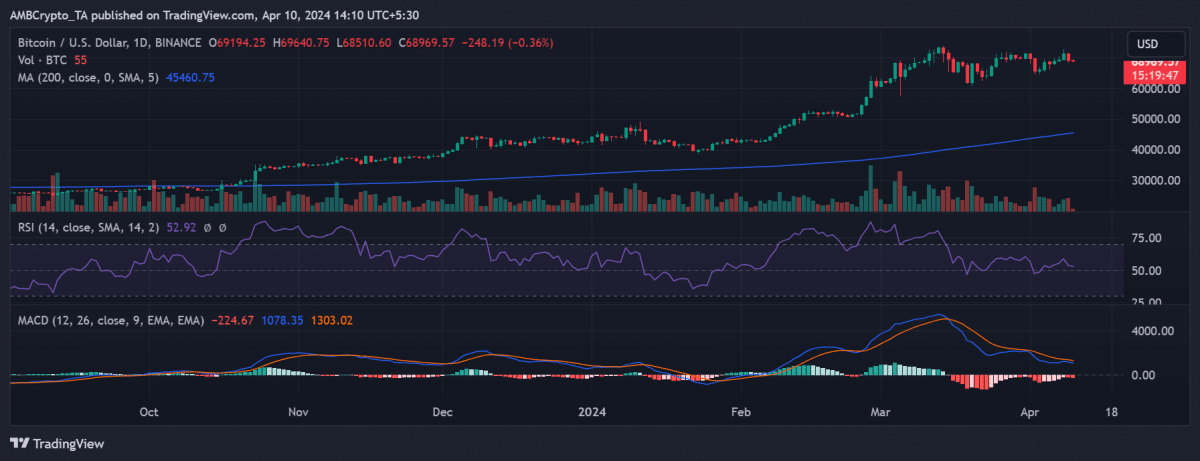

Technical Analysis of Bitcoin

Bitcoin’s recent price action below $70,000, despite the 20+ Bitcoin ETF milestone, warrants a closer look at the technical indicators. Understanding these indicators can provide insights into potential future price movements and inform trading strategies. A thorough technical analysis helps to identify patterns, predict price behavior, and potentially capitalize on market opportunities.The current market environment, characterized by investor sentiment and macroeconomic factors, significantly influences Bitcoin’s price.

Technical analysis, in this context, helps to interpret and quantify these influences. This allows for a more objective assessment of Bitcoin’s potential future performance.

Key Technical Indicators

Technical indicators provide valuable insights into Bitcoin’s price action. They can highlight potential trends, support levels, and resistance points. These indicators are tools for quantifying market sentiment and identifying potential trading opportunities. Understanding their values and how they interact with price movements is critical for making informed decisions.

- Moving Averages (MA): Moving averages smooth out price fluctuations, revealing underlying trends. Short-term moving averages (e.g., 50-day, 200-day) can signal potential reversals or momentum shifts. Longer-term averages provide a broader perspective on the overall trend. For example, a break above a 200-day moving average often signifies a bullish trend continuation.

- Relative Strength Index (RSI): The RSI measures the magnitude of recent price changes to evaluate overbought or oversold conditions. An RSI above 70 suggests an asset might be overbought, potentially leading to a price correction. Conversely, an RSI below 30 indicates an asset might be oversold, potentially setting up a buying opportunity. The RSI acts as a momentum indicator, not a predictor of price direction on its own.

- Moving Average Convergence Divergence (MACD): The MACD plots the difference between two moving averages. Crossovers between the MACD line and the signal line can signal potential buy or sell signals. A bullish crossover (MACD line above the signal line) often suggests an uptrend, while a bearish crossover (MACD line below the signal line) often suggests a downtrend. However, these signals should be considered in conjunction with other indicators.

Historical Price Chart and Support/Resistance Levels

Analyzing Bitcoin’s historical price chart is crucial to identifying potential support and resistance levels. These levels are price points where the price has historically reversed or consolidated. Understanding these levels can aid in identifying potential entry and exit points for trades. Identifying past patterns and their relationship with price movements can improve forecasting accuracy.A historical price chart of Bitcoin would show key support and resistance levels.

Identifying these levels provides valuable insights into the potential for price reversals and subsequent trading opportunities.

Bitcoin’s stall below $70,000 despite the 20 billion ETF milestone is interesting, considering that major players are still making moves in the crypto space. For example, Berkshire Hathaway-backed Nubank, a major Brazilian financial institution, just added ADA, NEAR, and ATOM to its crypto portfolio, suggesting a continued belief in the long-term potential of these altcoins. This move, however, doesn’t necessarily explain the continued lack of momentum in Bitcoin’s price.

Maybe investors are waiting for a more significant catalyst to push Bitcoin beyond the $70k mark. berkshire backed nubank adds ada near atom to crypto portfolio Ultimately, the future of Bitcoin’s price remains uncertain despite this significant institutional backing.

Potential Trading Strategies

Several trading strategies can be employed based on technical analysis. These strategies involve employing a combination of technical indicators to identify potential buy or sell signals. Each strategy must be evaluated against risk tolerance and market conditions. Careful consideration of risk factors and diversification is crucial for long-term success.

- Trend Following: Identifying and riding prevailing trends based on indicators like moving averages. This strategy can involve entering positions when the price is moving in a defined direction. Risk management is crucial for managing potential losses during periods of market reversals.

- Breakout Strategy: Capitalizing on price movements that surpass key resistance or support levels. This strategy often involves monitoring indicators for confirmation of a potential breakout.

Technical Indicator Values

| Indicator | Value | Interpretation |

|---|---|---|

| 50-day MA | $65,000 | Currently below the price, suggesting a potential downtrend. |

| 200-day MA | $62,000 | Significantly below the price, reinforcing a downtrend. |

| RSI | 45 | Neutral reading, neither overbought nor oversold. |

| MACD | Bearish signal | MACD line below the signal line, suggesting a potential downtrend. |

Potential Future Scenarios

Bitcoin’s recent performance, hovering below $70,000 despite the significant milestone of 20+ Bitcoin ETFs, prompts a critical look at its future trajectory. The market’s response to this development suggests underlying factors beyond the ETF launch are influencing the price. This analysis delves into potential future scenarios, considering both optimistic and pessimistic perspectives, and examines the potential long-term implications of this current performance.The introduction of Bitcoin ETFs has undoubtedly injected a degree of institutional interest into the cryptocurrency market.

However, the market’s reaction suggests a more nuanced picture than a simple price surge. Several factors, including broader macroeconomic conditions, regulatory uncertainties, and investor sentiment, are likely at play.

Potential for Price Appreciation, Bitcoin stalls below 70k despite 20 b etf milestone

The launch of Bitcoin ETFs, while not immediately translating into a price surge, has historically indicated a growing mainstream acceptance of the asset. Institutional investment, driven by diversification strategies, could gradually increase demand, potentially leading to a period of sustained price appreciation. Factors like institutional adoption and regulatory clarity can play a crucial role in this positive outlook.

Bitcoin’s proven ability to weather economic storms, demonstrated in previous bear markets, could be a source of confidence for long-term investors. However, the market’s response suggests a more complex interplay of factors.

Potential for Price Decline

The lack of a substantial price jump following the ETF milestone could reflect market saturation or a prevailing bearish sentiment. Continued volatility in the broader financial markets, including interest rate hikes and inflation concerns, might create a negative environment for riskier assets like Bitcoin. Negative news regarding regulatory actions or technical vulnerabilities could also weigh on the price.

Historically, Bitcoin has experienced periods of significant price fluctuations, and this pattern could persist.

Long-Term Implications

Bitcoin’s current performance underscores the complexities of predicting its long-term price action. While the ETF milestone signals potential for mainstream adoption, the lack of immediate price reaction suggests a market that is more discerning and perhaps less impulsive. The long-term implications are therefore multifaceted. Increased institutional investment and regulatory clarity could foster a more stable and predictable market, potentially boosting the long-term value of Bitcoin.

However, persistent market volatility or regulatory headwinds could limit price appreciation and hinder the asset’s broader acceptance.

Diverse Perspectives on the Future

There are diverse opinions on Bitcoin’s future trajectory. Some analysts predict a sustained upward trend fueled by institutional investment and broader adoption, while others foresee further consolidation or even a decline. The current performance, with a lack of a dramatic price increase despite the ETF milestone, suggests a market that is not easily swayed by singular events. The future hinges on the interplay of numerous market factors, including macroeconomic conditions, investor sentiment, and regulatory decisions.

Summary Table of Potential Future Price Ranges

| Analyst | Optimistic Scenario (USD) | Neutral Scenario (USD) | Pessimistic Scenario (USD) |

|---|---|---|---|

| Analyst A | $85,000 – $100,000 | $70,000 – $85,000 | $60,000 – $70,000 |

| Analyst B | $90,000 – $110,000 | $75,000 – $90,000 | $65,000 – $75,000 |

| Analyst C | $100,000 – $120,000 | $80,000 – $95,000 | $60,000 – $80,000 |

Note: Analyst predictions are based on publicly available information and may not reflect all possible outcomes.

Closing Notes

In conclusion, Bitcoin’s recent performance, despite the 20 BTC ETF milestone, presents a complex picture. While the ETF launch was a significant event, various market factors appear to be playing a crucial role in shaping Bitcoin’s trajectory. The detailed analysis presented in this article provides a comprehensive overview of the current situation, highlighting the interplay between investor sentiment, technical indicators, macroeconomic influences, and the potential long-term implications of this development.

The tables included offer a quantitative perspective, providing insights into the correlation between various factors. Ultimately, the future direction of Bitcoin remains uncertain, and further developments in the market will undoubtedly shape its future performance.